All Categories

Featured

Table of Contents

That's to avoid individuals from purchasing insurance right away after discovering an incurable health problem. This protection might still cover fatality from mishaps and other causes, so research the choices readily available to you.

When you assist relieve the economic concern, friends and family can concentrate on looking after themselves and organizing a purposeful memorial rather than rushing to find cash. With this kind of insurance coverage, your beneficiaries might not owe taxes on the fatality advantage, and the cash can approach whatever they need the majority of.

Best Funeral Expense Insurance

for modified entire life insurance policy Please wait while we recover info for you. To discover the items that are readily available please phone call 1-800-589-0929. Adjustment Area

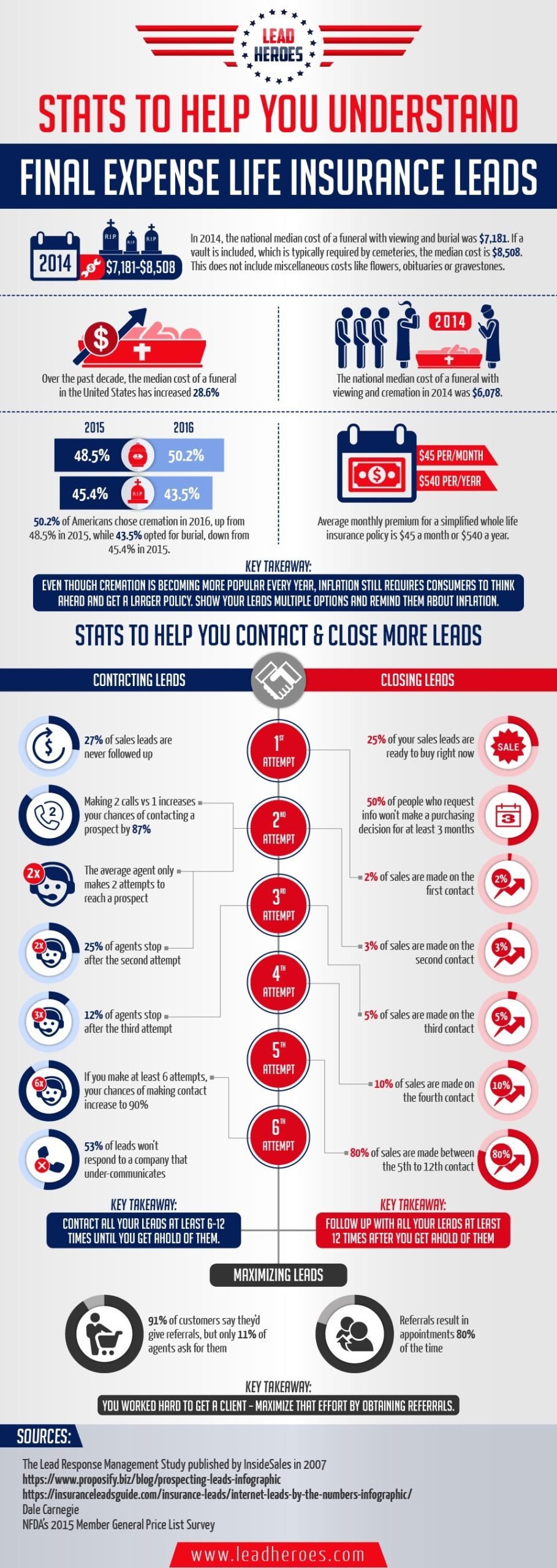

When you offer last expense insurance, you can supply your customers with the peace of mind that comes with recognizing they and their households are prepared for the future. All set to find out whatever you need to recognize to start selling final expense insurance coverage efficiently?

As opposed to offering earnings substitute for enjoyed ones (like the majority of life insurance coverage plans do), final cost insurance is implied to cover the prices related to the insurance holder's viewing, funeral, and cremation or interment. Legally, nevertheless, beneficiaries can typically use the policy's payment to pay for anything they wish. Generally, this type of plan is issued to individuals ages 50 to 85, however it can be issued to younger or older people.

There are four main types of final cost insurance policy: guaranteed concern, graded, modified, and level (liked or basic rating). We'll go more right into detail regarding each of these product types, but you can gain a fast understanding of the distinctions in between them through the table listed below. Specific benefits and payment routines might differ depending upon the carrier, strategy, and state.

Final Expense Protect Insurance

You're guaranteed protection however at the highest rate. Generally, guaranteed concern final expenditure plans are provided to customers with extreme or numerous wellness concerns that would certainly prevent them from securing insurance coverage at a basic or rated rating. what is a funeral policy. These wellness problems might consist of (however aren't limited to) kidney condition, HIV/AIDS, body organ transplant, active cancer cells therapies, and ailments that limit life span

Furthermore, clients for this sort of plan might have serious legal or criminal histories. It is essential to note that various providers offer a variety of concern ages on their assured problem policies as reduced as age 40 or as high as age 80. Some will likewise supply greater face worths, as much as $40,000, and others will certainly permit far better survivor benefit conditions by boosting the rates of interest with the return of costs or decreasing the number of years until a full fatality benefit is available.

If non-accidental fatality happens in year two, the service provider could only pay 70 percent of the survivor benefit. For a non-accidental death in year 3 or later on, the service provider would probably pay 100 percent of the fatality advantage. Modified final expense plans, comparable to graded plans, check out health and wellness problems that would put your customer in a much more limiting changed strategy.

Some items have particular health concerns that will certainly get favoritism from the provider. There are carriers that will issue plans to more youthful adults in their 20s or 30s who might have chronic problems like diabetes mellitus. Normally, level-benefit typical final cost or streamlined concern whole life plans have the cheapest premiums and the largest availability of extra bikers that customers can include to policies.

Real Insurance Funeral Cover

Depending on the insurance policy service provider, both a favored price course and basic price class may be supplied - final expense funeral insurance. A client in outstanding health and wellness without any present prescription medicines or wellness problems might get a favored rate course with the least expensive costs feasible. A client in great health and wellness also with a couple of maintenance drugs, but no substantial health and wellness problems might qualify for standard rates

Similar to various other life insurance policy policies, if your customers smoke, utilize other forms of cigarette or pure nicotine, have pre-existing health problems, or are male, they'll likely need to pay a greater rate for a final expenditure policy. Moreover, the older your client is, the higher their price for a plan will certainly be, given that insurance provider believe they're handling more danger when they offer to insure older customers.

Average Cost Of Final Expense Insurance

The policy will additionally stay in force as long as the insurance policy holder pays their costs(s). While lots of various other life insurance coverage policies might call for clinical tests, parameds, and participating in medical professional statements (APSs), last expense insurance policies do not.

To put it simply, there's little to no underwriting required! That being claimed, there are 2 primary kinds of underwriting for final expenditure plans: streamlined problem and guaranteed concern (omaha burial insurance). With streamlined concern strategies, customers usually just have to address a couple of medical-related questions and may be rejected protection by the carrier based upon those solutions

Funeral Protection Insurance

For one, this can enable representatives to identify what kind of plan underwriting would certainly function best for a specific client. And two, it assists agents limit their client's alternatives. Some providers may invalidate customers for coverage based on what medications they're taking and for how long or why they have actually been taking them (i.e., maintenance or treatment).

The short solution is no. A last expenditure life insurance policy policy is a kind of permanent life insurance policy - life insurance 10000. This suggests you're covered up until you pass away, as long as you've paid all your costs. While this policy is designed to aid your beneficiary pay for end-of-life expenditures, they are cost-free to utilize the death benefit for anything they need.

Much like any type of various other irreversible life plan, you'll pay a normal costs for a final cost plan for an agreed-upon fatality benefit at the end of your life. Each provider has different policies and alternatives, however it's reasonably easy to manage as your recipients will have a clear understanding of exactly how to spend the cash.

You may not require this kind of life insurance policy. If you have long-term life insurance policy in position your final expenses may already be covered. And, if you have a term life plan, you might have the ability to transform it to a permanent plan without a few of the additional actions of getting final cost coverage.

Affordable Funeral Policy

Developed to cover minimal insurance coverage needs, this kind of insurance policy can be a cost effective alternative for people who simply wish to cover funeral expenses. Some plans may have limitations, so it is important to review the small print to be sure the plan fits your demand. Yes, certainly. If you're searching for a permanent alternative, universal life (UL) insurance remains in location for your whole life, as long as you pay your costs. best burial insurance policy.

This choice to last expense coverage gives alternatives for added household insurance coverage when you need it and a smaller sized insurance coverage amount when you're older.

5 Vital realities to bear in mind Preparation for end of life is never pleasurable (burial life insurance companies). However neither is the idea of leaving enjoyed ones with unexpected expenditures or debts after you're gone. Oftentimes, these financial obligations can hold up the settling of your estate. Think about these 5 realities concerning last expenses and exactly how life insurance can help spend for them.

{kind=link}

Latest Posts

Insurance To Pay For Funeral Expenses

Affordable Burial Insurance For Seniors

How To Sell Final Expense Insurance